Setting aside the sinister photo on the recent cover story of Bloomberg Businessweek (a cheap stunt: US plant-based meat sales may not be red hot, but Beyond Meat patties were not grey, last time I checked), that article has attracted astonishing levels of praise—and vitriol—for simply stating what everyone following this space has known for months now: US retail sales of meat alternatives have slowed down and Beyond Meat has had a lousy year.

But scan the media today and plant-based meat is right up there with Meghan Markle (first they loved her, then they hated her), while proponents of cultivated meat are being likened to Theranos.

First—so we’re told—the tech bros were going to save the planet, but now they’ve been exposed as greedy chancers selling us processed mush and pipedreams, a view shared by some unlikely bedfellows from big meat companies to anti-GMO natural products companies, basking in schadenfreude with every piece of grim news emerging from Silicon Valley.

In this black-and-white world awash with false dichotomies, ‘fake’ burgers are pitted against ‘regenerative’ pasture-raised beef as if these are the only two choices, when the stated aim of pretty much every alt meat company I’ve ever interviewed is to reduce our reliance on factory farming, not to come after your organic grass-fed steak.

In this black-and-white world, ‘fake’ burgers are pitted against ‘regenerative’ pasture-raised beef as if these are the only two options

Has Beyond Meat lived up to its early promise? Not by a long shot. And is it likely—as Impossible Foods’ founder Dr. Pat Brown once predicted—that animal agriculture will be “eradicated” by 2035? I doubt it, although I’ve never come across anyone who took this claim literally, including, I suspect, Dr. Brown himself.

So is plant-based meat a ‘fad’ and a ‘flop’ as Bloomberg Businessweek asserts?

I certainly hope not, given that attempts to persuade us to swap our cheap burgers and fries for chickpea curries aren’t going well. This doesn’t mean we shouldn’t embrace whole food plant-based culinary traditions, just that Impossible Burgers and Channa Masala may both be valid items on the menu.

Meanwhile, grass-fed beef—apparently the answer to all of our problems if you follow this debate on social media—is not going to meet demand unless we have a couple of planets to spare or convince people to slash their meat consumption, according to research from New York University.

Enlightened policymakers in some countries are advocating for the latter, but if you’re expecting to see this recommendation in the next edition of the USDA’s Dietary Guidelines, don’t hold your breath.

So let’s ditch the binary thinking and acknowledge that there are no silver bullets when it comes to reducing our reliance on animal agriculture, a leading driver of climate change and deforestation, antibiotic resistance, and habitat destruction and that we have to explore multiple strategies.

Animal foods don’t have to be the visual, nutritional, or sensory benchmarks for human food

One such strategy is reverse engineering meat, and I have little doubt that over time, as the technology improves and prices come down, plant-based, fermentation-based, and cultivated meat analogs will gain more traction with consumers, who crave the taste, texture, and aroma of meat, not industrial-scale slaughter.

But straight analogs are not the only game in town.

For consumers who think reverse-engineering the western diet shows both a lack of imagination and a disregard for human health, there is a world of possibility for food companies to make a more diverse range of foods inspired by plant-based culinary traditions, and to create new center-plate protein-based options that are tasty and satisfying, but don’t look or taste like animal foods at all.

Pork, chicken, beef, tuna, shrimp, cow’s milk, and chicken eggs don’t have to be the visual, nutritional, or sensory benchmarks for human food; they’re just products our agricultural system has become extremely efficient at producing at scale.

There are scores of foods in our homes today that we weren’t eating 10 years ago, never mind 100 years ago

Fast forward to 2123, and who knows what we’ll be eating. There are strains of fungi out there with as much protein as beef, a ton of fiber, no saturated fat, and lots of B vitamins, which can be grown with a fraction of beef’s environmental impact; perhaps these will become dietary staples.

In 2123, milk from lactating ruminants may have to be labeled as ‘cow’s milk’ because it’s no longer the default. Maybe the word ‘milk’ will disappear altogether.

There are scores of foods in our homes today that we weren’t eating 10 years ago, never mind 100 years ago, so the notion that we’re stuck with the status quo just because Beyond Burgers have not met expectations in the US market shows a certain lack of imagination.

Oat milk barely registered in the plant-based milk data in the US five years ago and now it’s #2 behind almond milk and is driving the bulk of the growth in the category. Some consumer habits change surprisingly quickly.

Meat analogs were not invented in Silicon Valley in 2010

So back to alt meat. If it’s a fad, it’s a pretty long-standing fad. Meat analogs – not just bean burgers as some media outlets keep repeating – were not invented in Silicon Valley in 2010.

Tofu has been around since the Han Dynasty; Dr. John Harvey Kellogg started serving soy- and peanut-based ‘meat’ at the Battle Creek Sanitarium in the 19th century; NASA was experimenting with growing meat from microbes in the 1960s; ADM’s textured vegetable protein was popularized in the 1970s; and Quorn’s fungi-based meat has been on sale since the 1980s.

For some pioneers, the impetus was health, for some, animal welfare, while others simply felt there were smarter ways to feed people on a planet with finite resources than slaughtering billions of farm animals.

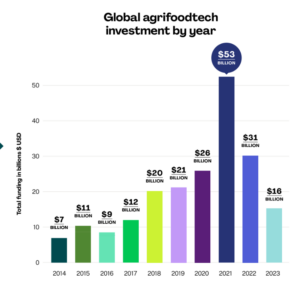

With this in mind, you can bet that all of the world’s biggest food companies from Nestlé and Unilever to JBS and Cargill are still very much following this so-called ‘fad,’ in spite of slowing US retail sales—and the corresponding drop in investment.

Plant-based meat: Test and learn

Today, plant-based meat or dairy alternatives are in every leading food retailer and half of US restaurants compared with a third in 2012, while all the leading fast-food brands, restaurant chains, and coffee chains are experimenting to see what resonates with their clientele.

Has McDonald’s instituted a nationwide rollout of Beyond Burgers in the US market? No. Does this mean the world’s largest fast-food brand has ‘given up’ on meat alternatives? I very much doubt it.

Has Taco Bell gone national with a leading alt-meat brand? Not yet; it’s still trying to find what resonates with its customers, just like every other restaurant chain. But the underlying drivers behind these tests haven’t changed, and if companies want to meet environmental goals — particularly those that are publicly-listed and under pressure to feature on ESG stock indexes — if nothing else, they will need to keep exploring meat alternatives.

US retail sales of plant-based meat have hit a wall, but they haven’t fallen off a cliff

As for the US retail market data, while overall sales of meat alternatives have slowed dramatically following a surge in the early months of the pandemic, the category hasn’t fallen off a cliff. However, it appears to have hit a wall — dollar sales were flat in 2022, with units down -8.2% year-on-year, according to IRI data crunched by 210 Analytics* (*see below).

A ‘flop’? It looks more like a crisis of confidence driven by investors getting ahead of themselves and banking on a hockey stick growth curve instead of a mild incline.

Ultra-processed fake meat… a red herring?

There are plenty of credible explanations for the slowdown, with some commentators highlighting sub-par taste and texture and over-saturation with me-too products, some pointing to hard-wired cultural barriers (Americans love meat), and some saying the slump is simply a natural correction following a period of rapid trial in the early months of the pandemic.

Another argument made repeatedly is that alt meat products don’t appeal to meat eaters because they are too ‘processed’ or not obviously healthier than the products they are replacing.

This, however, becomes more problematic once you start looking at the data, where there is not an obvious correlation between shorter, cleaner ingredient decks or sodium and saturated fat levels, and sales performance.

Beyond Meat has less saturated fat than most rivals; Lightlife told shoppers its meat was made in a kitchen, not a lab (which didn’t persuade people to buy more of it); and Planterra’s OZO brand had the lowest saturated fat and one of the ‘cleanest’ ingredient lists in the category, but was axed by parent company JBS nonetheless.

If health was the primary factor motivating plant-based milk purchases, soymilk would still be the market leader in the US, rather than almond and oat milk.

Americans eat plenty of highly processed packaged foods with long lists of ingredients you won’t find in Grandma’s kitchen because they deliver a consumer benefit

As for consumer survey data on ‘ultra-processed’ foods, it’s not hugely illuminating. We all buy scores of processed foods with ingredients you won’t find in Grandma’s kitchen (allulose, Reb M, mono- and diglycerides) because they deliver a consumer benefit, whether it’s a ‘sugar-free’ positioning or no oil slick at the top of your jar of peanut butter.

Would consumers prefer products made only with ‘kitchen cupboard’ ingredients? Of course. Would sales of alt meat suddenly take off if everyone ditched methylcellulose or titanium dioxide? I doubt it.

Price: Not the whole story?

As for price, it’s undoubtedly holding the market back in the current inflationary climate, but it’s probably not the whole story.

As a case in point, Daring Foods—a premium brand that uses high-moisture extrusion to make plant-based chicken with a handful of ingredients—is performing well while some lower-priced rivals are struggling.

Solve a problem for consumers today… and tomorrow

Above all, whether you’re making plant-based burgers or bean-free coffee, you still have to hit the right buttons on taste, value (which isn’t the same as price) and convenience; you have to have a compelling brand, great execution, and a clear understanding of what problem you’re solving for your target consumer today, as well as tomorrow.

Having a long-term mission—and talking passionately about how you’re tackling structural problems in the food system from deforestation to drought—is important, but in the current economic climate of food inflation and layoffs in various sectors, it may not be enough to warrant a price premium unless you’re also hitting all of the other hot button issues above.

Let’s face it, most people—including those who care about climate change—have more immediate priorities when they’re shopping: is this good value, will my kids eat it, is it better for me, is it easy to cook?.

So brands must give consumers more immediate reasons to buy, as well as something they can feel warm and fuzzy about afterwards — ‘I made a better choice for the environment/animals‘.

Plant-based milk and plant-based meat are not the same

Indeed, one reason I suspect plant-based milks have achieved greater household penetration than plant-based meats, apart from the fact that they’re easier to make, is that they offer multiple immediate purchase drivers that have nothing to do with saving the planet.

And most of them taste nothing like dairy milk. In some cases, that’s actually why people buy them, underlining again that precise mimicry doesn’t have to be the goal for every brand.

Maybe you’ve started drinking oat milk with coffee because you tried it in a coffee shop and had a good experience. Maybe you drink almond milk because it has fewer calories. Maybe you prefer the taste. Maybe you’re avoiding lactose, or your kids have a milk protein allergy.

If you can also feel good about your purchase afterwards because it’s better for the planet, great, but let’s be honest, it’s probably not the main reason you bought it (if that were true, we’d all be vegans).

Branding and messaging

Brands that succeed understand their strengths, weaknesses, and their target consumers. For example, in the US plant-based cheese category, Miyoko’s Creamery has built a strong following for its artisanal cultured nut products.

However, a jump into more processed American-style alt-cheese slices didn’t work for Miyoko’s, in part because the products didn’t deliver, but also because it didn’t make sense for the brand, which has strong culinary credentials.

For alt meat players in the fresh meat case, meanwhile, a commoditized category dominated by private labels, if the best you can do is offer something not quite as appealing as what’s already out there (conventional meat) for almost twice the price, it’s probably not surprising that sales are heading in the wrong direction.

Making the case for plant-based meat

But this isn’t a reason to despair. There is an enormous opportunity to drive supply chain efficiencies and create more appealing products, but also to create more compelling brands and messages to draw attention to products that deliver a solid value proposition to the consumer.

There’s no ‘Got Milk’ campaign for meat alternatives. But if enterprising food marketers can persuade consumers to pay dollars for something most households have on tap in their own kitchen for cents (bottled water in single use packaging, backed by celebrity investors touting their green bona fides, no less), surely there are creative ways to make the case for plant-based meat, which is at least attempting to address an environmental problem, rather than creating a new one?

Impossible Foods: ‘The plant-based meat category has done a lousy job of explaining itself’

As Impossible Foods CEO Peter McGuinness—a marketer by trade—has pointed out, when it comes to selling meat alternatives to the mainstream, “The category has done a lousy job of explaining itself,” he told me last year.

No one, he claims, “other than in keynote speeches and lobbying efforts is saying in a mass, compelling way, that these products are better for you and the planet. When you talk to people about the planet, they still tend to talk about electric cars or recycling, rather than their food choices. I honestly think this is one of the biggest communication challenges in food.”

As delegates were told at a recent cellular agriculture event organized by Tufts University, success in the meat alternatives field is by no means inevitable, and many companies may well run out of cash before these products make any real dent in protein supply.

But as Uma Valeti, founder of cultivated meat co UPSIDE Foods, also noted at the event, unless the naysayers present a credible plan B, all that pioneers in this space can do is keep calm, carry on, and try and make the future happen.

“Talk is cheap. So let’s prioritize action… take the constructive criticism, but keep moving forward.”

What do you think? Email me at [email protected].

Sponsored

International Fresh Produce Association launches year 3 of its produce accelerator